As property transactions continue to rise against a backdrop of still-low new listings hitting the market, sellers may slowly gain an upper hand as available stock shrinks to the lowest levels in over a year in most markets.

CoreLogic NZ’s Monthly Housing Chart Pack, released today, shows residential sales numbers (via estate agents and private transactions) have increased for four consecutive months, with August’s figure up 5.5% on a year ago.

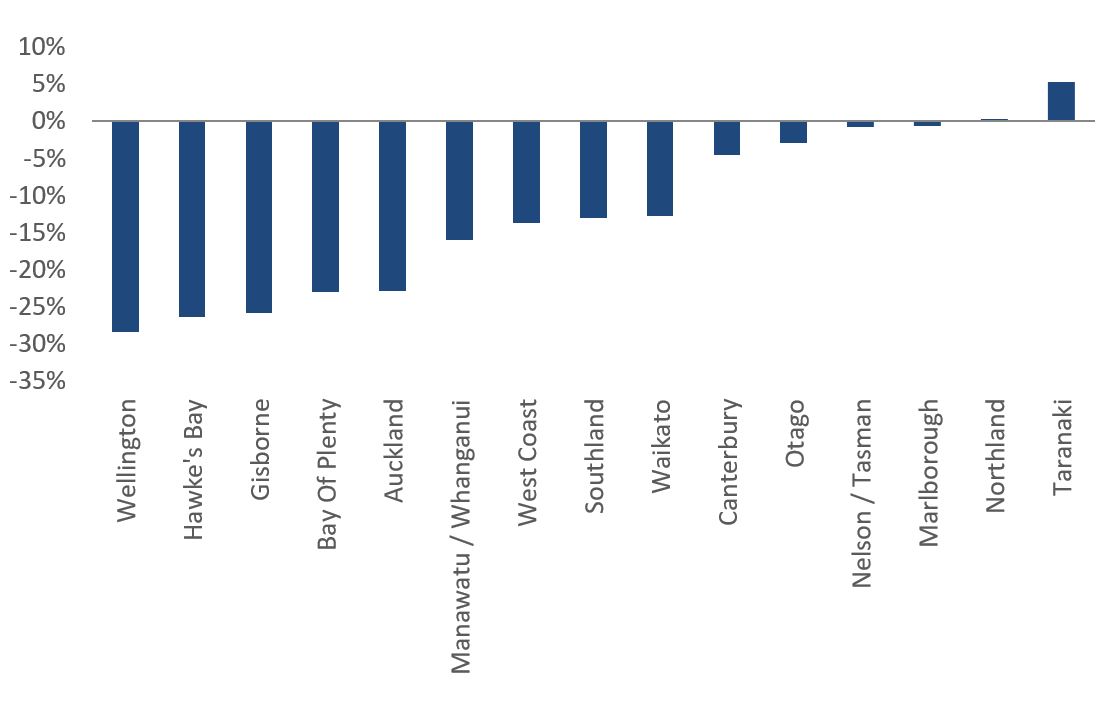

In contrast, the new listings count over the four weeks ending 10 September was 6,602, which is 18-19% below the same time last year and the five-year average.

CoreLogic NZ Chief Property Economist Kelvin Davidson said this emerging mismatch between supply and demand will start to place some upwards pressure on prices – although it could still be fairly muted by past standards.

“August marked the fourth consecutive monthly rise in sales volumes, and while the increase is off a low base of around 60,000 annual sales versus a longer-term average of around 90,000 annual sales, upturns have to start somewhere,” Mr Davidson said.

“Factors such as a broad peak for mortgage rates and strong net migration suggest that is what’s happening right now. On the supply side, the ‘spring lift’ has begun, but the flow of new listings coming onto the market each week is still well below average as would-be vendors choose to ‘wait and see’, given the uncertainty about how long a sale might take and/or the potential price achieved.

“Arguably it remains a ‘buyer’s market’, with the national total stock of listings on the market still relatively high. However, there is a downwards trend now evident for stock levels too, which may start to contribute to competitive price pressures.”

Latest total listings count vs same time last year

The latest Buyer Classification data shows first home buyers remain active, with about 27% of property purchases in August, a record high. On the flipside, relocating owner-occupiers or ‘movers’, and mortgaged multiple property owners (MPOs) are less active than usual.

“First home buyers are enjoying lower house prices, less competition from other buyer groups, and also some other supports – such as KiwiSaver for the deposit, First Home Grants/Loans, and access to low-deposit finance via the LVR speed limits,” Mr Davidson said.

“Mortgaged MPOs activity is at record lows, being restrained by the required 35% deposits, low rental yields, and lack of mortgage interest deductibility.

Rental growth is also starting to show signs of a clear upturn, with both the Stats NZ and MBIE measures now accelerating, reflecting further growth in wages and a tightening supply/demand balance in the rental sector. However, the pace of growth may be constrained by the already-high starting point for the level of rents in relation to household incomes.

Overall, Mr Davidson said August brought more evidence that the housing downturn has found a floor and the next phase is slowly emerging.

“We’re still pretty cautious about the potential speed of any upturn. After all, while strong net migration and high employment are supportive, mortgage rates are still high – and unlikely to fall for at least another year.

“Housing affordability remains stretched and caps on debt to income ratios for mortgage lending loom next year. On balance, house price growth in the coming year or two could well be weaker than in past ‘rebounds’,” Mr Davidson said.

September Housing Chart Pack highlights:

- Residential real estate is worth $1.56 trillion.

- Nationally values fell by -8.7% in the year to August, a deceleration from the figures of greater than 10% from March through to July.

- Some key parts of Auckland and Wellington actually saw values rise in August (as well as July).

- The number of property sales in August was 5.5% higher than a year ago, the fourth consecutive monthly increase.

- There were 6,602 new listings over the four weeks ending 10 September, down from 8,144 this period last year.

- Total stock on market is 30,634, around 15% below this time last year.

- First home buyers’ market share of 27% remains strong, particularly in Wellington and Auckland at 33% and 29% respectively.

- Nationally rental growth hit 6.2% in August, and could remain elevated as net migration increases and rental stock stays low.

- Gross rental yields nationally have edged back up to 3.1% (from a trough of 2.6% for much of 2022), the highest level since early 2021.

- Around 53% of NZ’s existing mortgages by value are currently fixed but due to reprice onto a new (generally higher) mortgage rate over the next 12 months.

- Inflation seems to have passed its peak and the Reserve Bank will wait to see the effects of the 5.5% OCR for this tightening cycle. Mortgage rates are close to, or already at, their peak.

Download the Housing Chart Pack

CoreLogic New Zealand