CoreLogic's House Price Index (HPI), which is the most complete and robust measure of property value change in the market, shows some momentum remains in the property market, however uncertainty caused by tougher lending criteria and higher mortgage rates, as well as the current Omicron outbreak, is producing some diversity in the results.

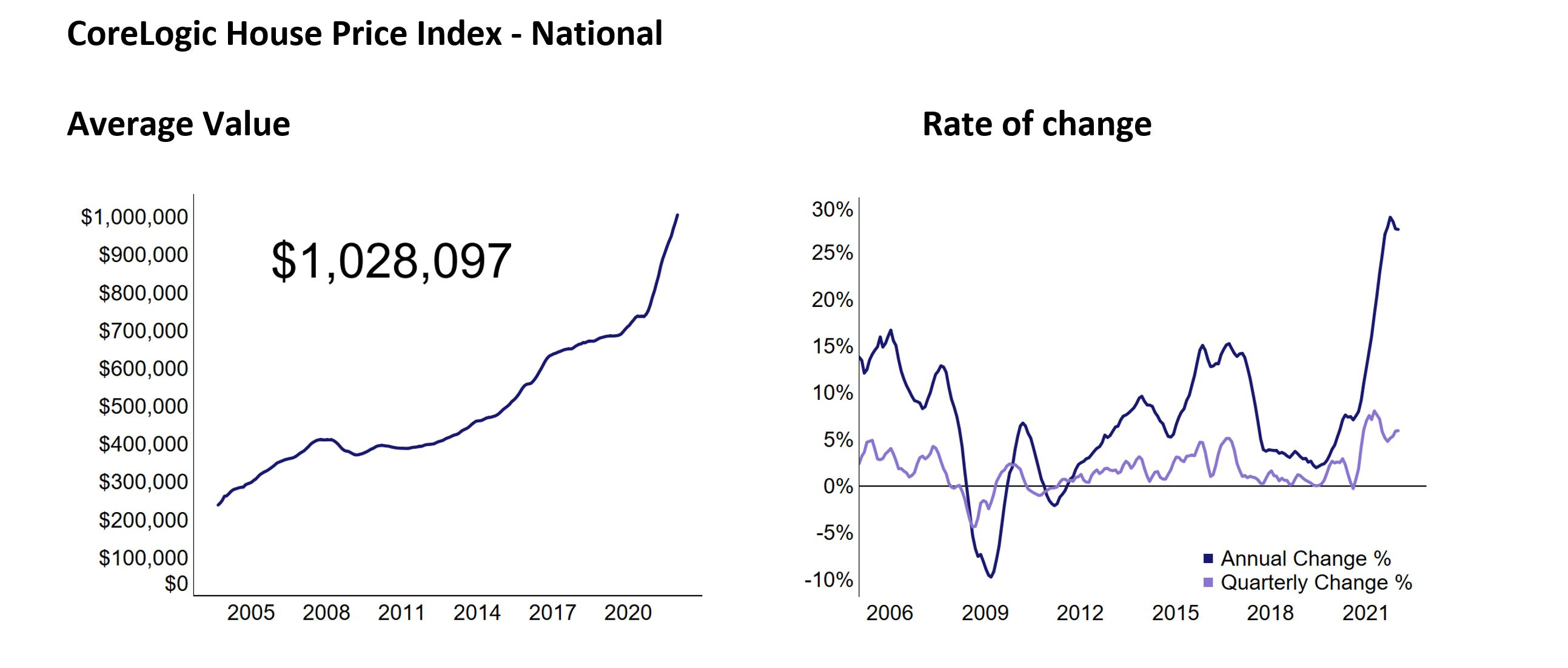

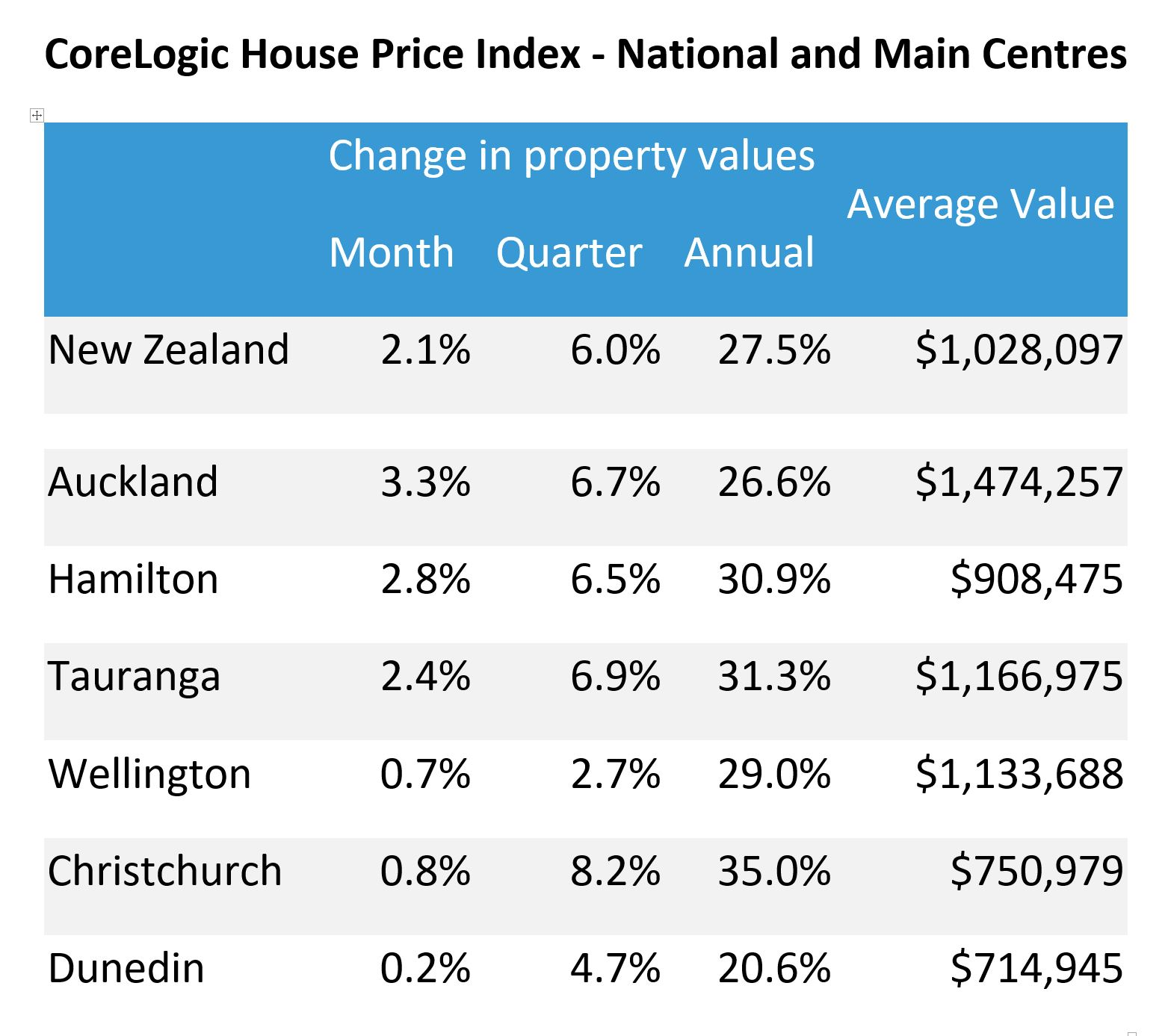

Nationally, property values rose 2.1% over January, a slight increase on December's rate of growth (1.9%).

Following this period of volatility (also affected by the seasonal summer slowdown), there is mounting evidence residential property values could slow in the coming months with some areas more vulnerable than others. Certainly, property market activity levels seem to have passed their peak, and typically that will lead to a clearer slowdown in values after a lag of a few months.

CoreLogic NZ Head of Research Nick Goodall said: "The shift to red in Aotearoa's COVID-management plan brings another layer of uncertainty to the market, but with the increased difficulty to secure finance being the lead topic and probably greatest influence over the future of the market right now, the impact of social restrictions is likely to be minimal.”

Following overwhelming feedback that recent changes to the Credit Contract and Consumer Finance Act (CCCFA) had gone too far and were unnecessarily impacting the ability of credit-worthy borrowers to secure mortgages, the Government has asked the Council of Financial Regulators to review the regulations and investigate whether lenders are implementing the new rules as intended.

"The difficulty for the regulators will be to disentangle the impact of the CCCFA changes, alongside tighter loan-to-value ratio (LVR) restrictions, which have further limited the volume of high-LVR loans, and increasing interest rates, which have impacted borrower affordability,” Mr Goodall said.

Mr Goodall said a minor reduction in the annual rate of growth, to 27.5% (from 27.6% at the end of December), illustrated some momentum remains in the market, however conditions are very different to the same time a year ago when persistently high buyer demand, assisted by low interest rates and low advertised supply saw value growth rapidly accelerate.

Recent economic data, including CPI figures for December strengthen the case for another increase in the OCR (currently 0.75%) at the next Reserve Bank review on 23 February. The likelihood of a 0.5% increase rather than a 0.25% increase has also grown stronger. If this month's Q4 labour market figures are also as strong as expected (unemployment may even drop again), the OCR hike seems almost certain.

"This underlying strength in employment similarly provides the basis of our expectation that a significant downturn is unlikely. Home owners have had their mortgage resilience tested at higher interest rates and they are likely to adjust other areas of their spending before missing mortgage payments. Unless they lose their job or a significant proportion of their income they are unlikely to want to sell their property,” Mr Goodall said.

"Investors may have more to consider as they file their first part-year tax return with interest costs not included, however a larger tax bill for any capital gain made for those who have owned their asset for less than five years may provide a greater deterrent to selling. Meanwhile for those in the market more than five years, their mortgage and interest costs will likely pale in comparison to the value of their property and with rental growth exceeding 5% in the past year, many investors should have adjusted for the parallel increase in costs.”

This should guard against a massive investor sell-off, however the tighter tax rules, alongside reduced accessibility to credit, diminished affordability and low gross yields, could have a material impact on demand from this section of the market, especially for existing (non-new) properties. Indeed, RBNZ lending data for December showed the drop in lending compared to 2020 data was almost entirely from investors, with owner occupiers flat year-on-year.

Perhaps the most intriguing trend to watch for the year will be the potential for the slow-down or downturn to play out differently throughout the regions. Available listings will play a key part in this with some cities having more than double the amount of properties listed for sale now than the prior year (Lower Hutt, Palmerston North), while others continue to have fewer (Whangārei, Queenstown).

The mixed results were evident across the main centres. The rate of growth in Auckland strengthened on all measures (three, six and 12 months) while the phenomenal recent growth witnessed in Christchurch appears to have run its course, with the annual growth rate dropping from 38.0% at the end of December 2021 to 35.0% at the end of January 2022.

The average property value in Hamilton now exceeds $900,000, hitting $908k at the end of January, and the annual rate of growth in Tauranga increased to 31.3%, despite gradually slowing since October 2021.

The annual rate of growth in Dunedin is the lowest of the six main centres, sitting at 20.8% for the 12 months to the end of January. The rate of growth for Wellington property reduced across all three measures with the annual rate (29%) declining for the third month in a row (from 36% in October 2021).

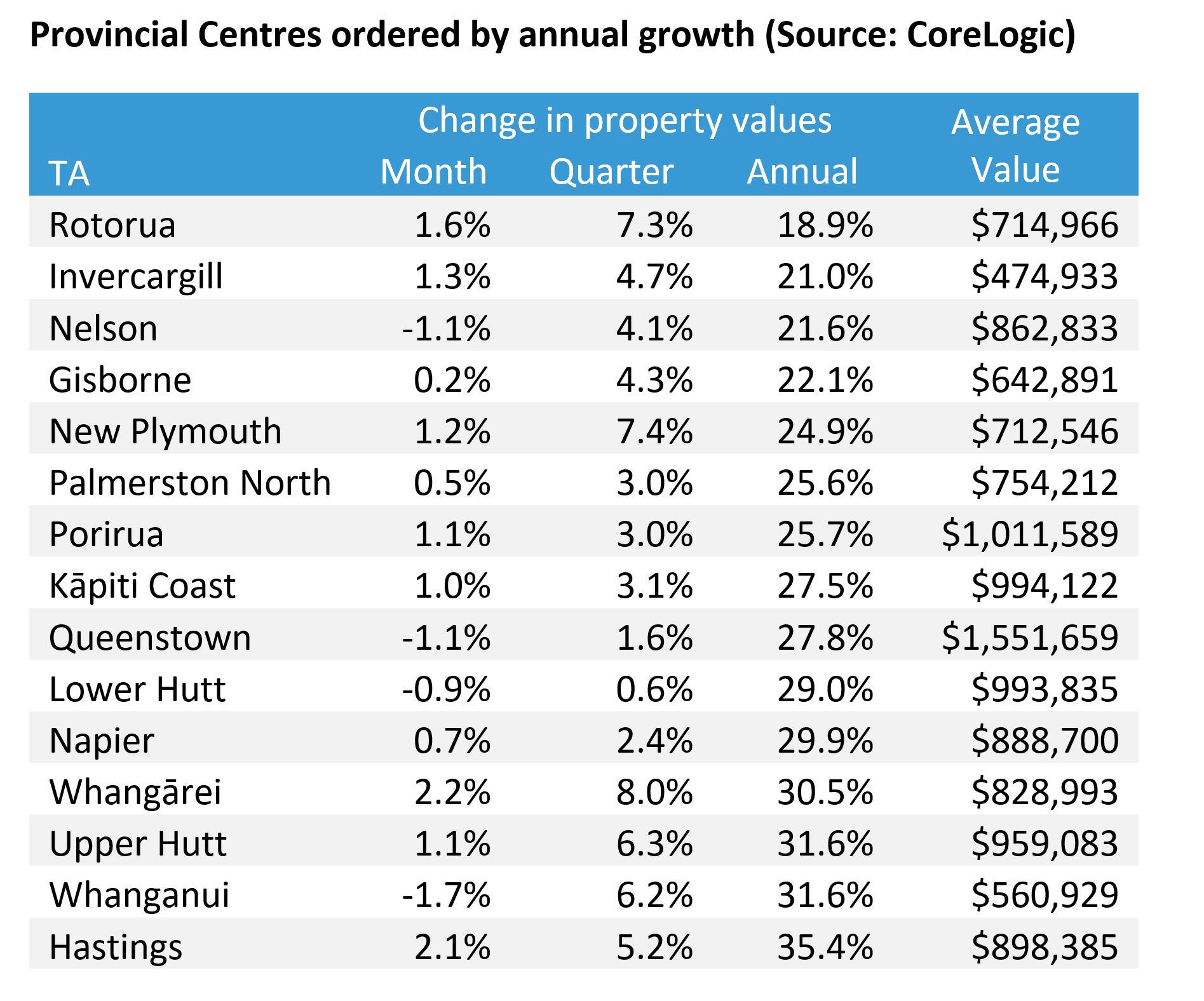

All but one of the provincial centres tracked saw a reduction in the annual rate of growth. In Rotorua the rate increased from 18.2% to 18.9%, which remains the lowest of these centres.

In Whanganui the rate dropped from 37.0% to 31.6%, while Kāpiti Coast (from 32.0% to 27.5%), Gisborne (24.7% to 21.0%) and Lower Hutt (33.6% to 29.9%) also saw the annual rates of growth reduce by more than 3.5%.

Property values dropped -1.1% in Queenstown for the second month in a row, possibly a reflection of the centre's $1.57 million average property price and the impact of declining affordability and restricted credit.

Values in Whanganui saw the greatest drop (-1.7%) over the month, while Nelson (-1.1%) and Lower Hutt (-0.9%) also saw values fall. In Lower Hutt, values are below $1 million ($993k) after hitting the milestone for the first time at the end of December 2021.

Note:

The CoreLogic HPI uses a rolling three-month collection of sales data. This has always been the case and ensures a large sample of sales data is used to measure value change over time. This does mean the measure can be less reactive to recent market movements but offers a smooth trend over time. However, due to having agent and non-agent sales included, the index provides the most comprehensive measure of property value change over the longer term.

DOWNLOAD THE JANUARY HPI

Enquire about the CoreLogic House Price Index, request a copy of the latest data or subscribe to future updates here.

Meet Nick Goodall

Head of Research

Nick is an ace with numbers, and he has a knack for transforming facts and figures into compelling stories to inform a wide range of audiences. As our Head of Research, Nick is at the forefront of the latest trends driving the NZ property market.

Full profile