In today's Market Pulse, Chief Property Economist Kelvin Davidson dives into lending activity and shares 10 key insights about mortgage debt across the country.

The housing loan market has been relatively subdued over the past 12-18 months, alongside the downturn in sales volumes and property prices. But there are now signs of a turnaround for those variables, and lending activity is also starting to rise – albeit from a low base. So what’s the current lie of the land and what are key things to keep in mind?

1. New lending flows over August-October were 4% higher than a year ago.

The Reserve Bank figures show gross new lending flows for house purchases, bank switches and loan top-ups over August-October were 4% higher than a year ago, but the total of $16.8bn was still well below the figures for the same period in both 2020 and 2021, of $21.9bn and $22.8bn respectively.

2. Loan to value ratio rules are still biting fairly hard.

Only 0.3% of investors got a loan in October with less than a 35% deposit, and only about 7% of all owner-occupiers (FHBs and existing owners) borrowed at less than a 20% deposit. The allowable cap, or speed limit, for that low deposit owner-occupier lending is 15%.

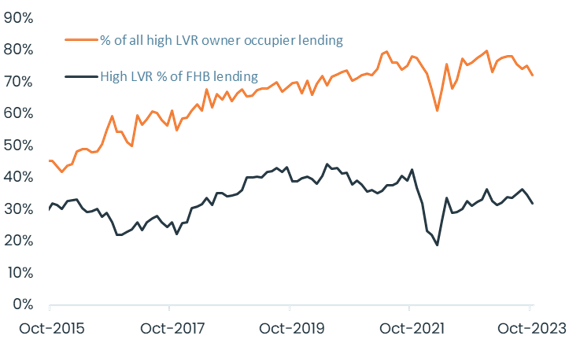

3. First home buyers (FHBs), however, are certainly capitalising on the speed limit.

Around one-third of FHBs who got a loan in October did so at low deposit (or high LVR), and they’ve fairly consistently been accounting for 70-80% of all owner-occupier lending at a low deposit.

High LVR first home buyer lending

4. FHBs also take out relatively large loans.

The average in October was just short of $562,000, versus the investor figure of around $493,000.

5. So-called ‘risky’ lending is not much of a problem at present.

Only around 17% of lending in October was interest-only (versus figures of as much as 40% in the past), and loans at debt to income (DTI) ratios of at least seven are also ‘under control’. That DTI bucket has accounted for only about 1% of FHB loans recently, and less than 8% for investors. Through 2021, those same figures for investors were typically 35-40%. The key handbrake here is simply high mortgage rates, which naturally limit the amount of debt that can be secured/serviced.

6. Indeed, the latest industry-wide figure for a ‘special’ (high equity) one-year fix was about 7.3% and the two year rate is roughly 7%.

The lows for those rates were 2.2% and 2.6% respectively. Across the stock of existing debt right now, the average mortgage rate is 5.3%, up from the trough of 2.7%, but still well below prevailing market rates

7. Total mortgage debt currently stands at $354bn, versus an estimated value of our property stock of $1,585bn.

That’s an aggregate LVR of only around 22%, implying there’s a lot equity out there (at least on paper).

8. Even so, the mortgage repricing process is ongoing and will remain a key issue in 2024.

About 54% of current loans are fixed but due to be repriced in the next 12 months, many of which will see a higher mortgage rate. Indeed, recall from #6 that average existing rates are still well below current market rates.

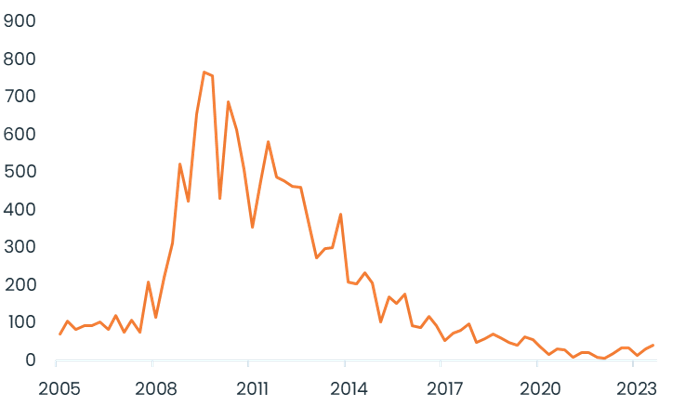

9. Amongst the existing loans, however, at least non-performing mortgages remain very low, at less than 0.5% of the value of debt.

Our own CoreLogic data also shows that mortgagee sales are at low levels too, just 41 in Q3 2023 (see the second chart below). To be fair, no mortgagee sale can be a good thing. But at least they’re far lower than the post-GFC period.

Mortgagee sales per quarter

Source: CoreLogic

10. It’s also encouraging that many existing mortgage-holders are ahead on their repayments.

Recent Westpac data, for example, shows that on their books, about two-thirds of borrowers are at least three months in the black, with a median buffer of nearly $13,000. This pattern is likely to apply to the other banks too. Of course, we also need to acknowledge recent Centrix data showing that there are around 19,000 mortgage accounts past due – up by 25% from a year ago, but from a very low base.

So what are the key takeaways here? First, the labour market has been robust in the past few years, even though the economy has been flirting with recession. That job security has kept stress in the mortgage sector at low levels, even though households have had to significantly adjust their finances.

Second, however, that reassuring trend of households steadily adjusting to higher mortgage rates may not last forever, especially if we do see some job losses in 2024. The mortgage repricing issue remains a key one to watch. Third, and more generally, the ‘post-COVID’ years have reinforced the key role of credit availability and cost in driving short-run trends in the housing market – the boom in 2020-21 when mortgage rates fell, and then the subsequent downturn as rates rose.

Of course, migration, population changes, and housing supply are vital factors in the medium/long term. But due to ‘higher for longer’ mortgage rates, we remain cautious about the potential speed of this emerging ‘upturn’ in house prices. Certainly, high interest rates – combined with low rental yields – are a key hurdle for investors looking to expand or start their portfolios at present.

Meet Kelvin Davidson

Chief Economist

Kelvin joined CoreLogic in March 2018 as Senior Research Analyst, before moving into his current role of Chief Economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Full profile