If you're looking for one part of the housing market jigsaw to really keep an eye on this year, you wouldn't go too far wrong with the mortgage sector. With interest rates higher, regulatory pressures still in force, and a large number of borrowers needing to refinance an existing fixed loan this year, it's all action.

Certainly, the latest lending figures from the Reserve Bank showed another sluggish month in February, with low-deposit first home buyers (FHBs) feeling the pinch. The outlook for 2022 is looking a lot weaker than 2021.

The Reserve Bank's latest figures show that mortgage lending flows were soft again in February, with the total of $5.7bn about $1.9bn lower than a year earlier. Investors accounted for most (-$1.3bn) of that drop, which isn't a surprise given that the past 12 months have seen the landscape change significantly, with deposit requirements increased, tax changes introduced, and rising mortgage rates meaning that some previously cashflow-positive properties won't be that way now.

However, owner-occupiers aren't as busy either, seeing lending flows drop by -$0.6bn over the past year. In particular, the figures show that low-deposit FHBs continued to have a tough time in February, with just 22% of all lending to FHBs going out at less than a 20% deposit, it wasn't long ago that this figure was more than 40%.

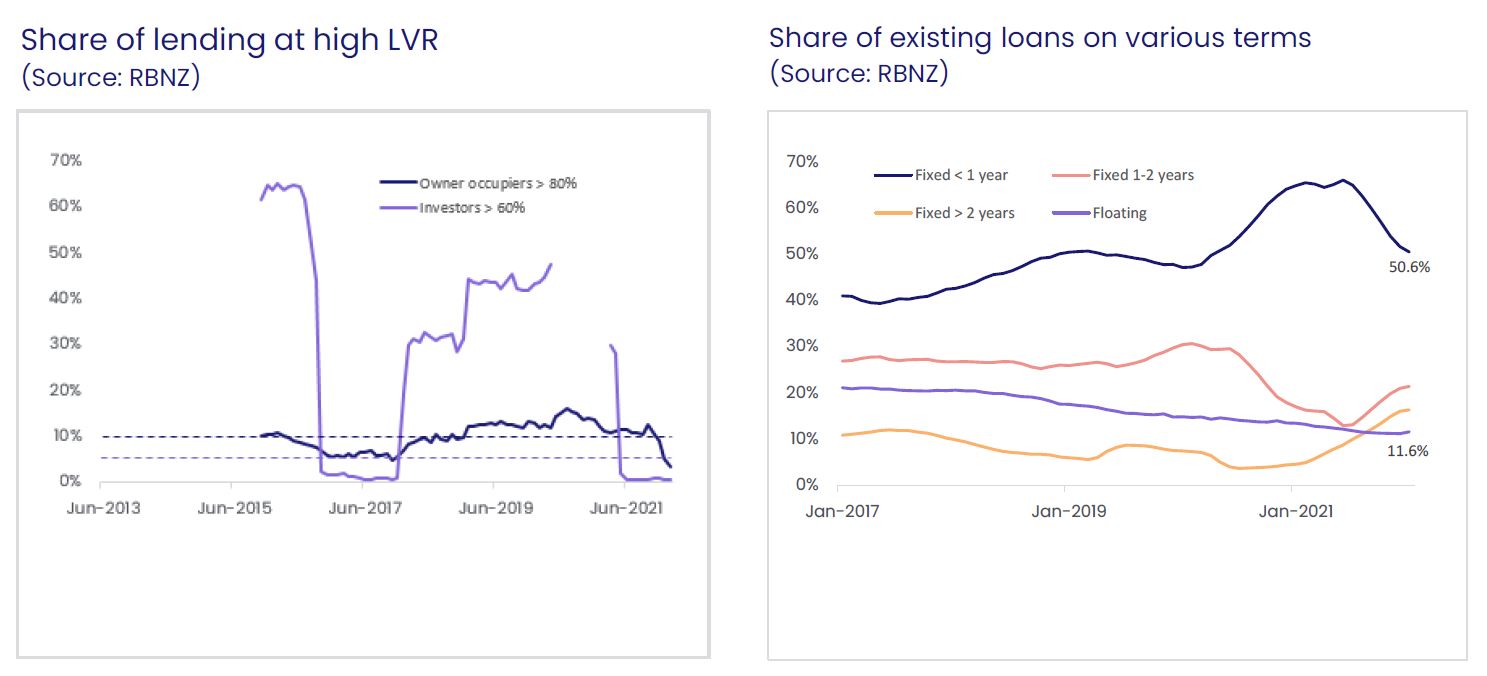

One obvious reason for this is simply that the LVR rules were tightened on 1 November, and FHBs were previously the key users of the higher speed limit. As the second chart shows, banks are currently operating well below the speed limit (as per past experience of liking to keep a buffer between theory and reality), and in fact in February, just 3.4% of owner occupier loans were approved with less than a 20% deposit – well below the 10% cap.

We're also keeping a running watch on the options borrowers are taking when it comes time to refix their existing loans, and as the third chart shows, the trend towards fixed periods of one to two years and longer than two years continued in February, with the share of all loans currently fixed but due to roll over in the next 12 months falling further. That said, the share of loans that need to be refinanced this year (51%) is still pretty significant, and these borrowers are going to be rolling off lower rates into a rising interest rate environment.

Overall, there weren't too many surprises in the latest mortgage data, not least because we already knew that sales activity itself was low in February (hence it was inevitable that mortgage flows would also be soft), and also from our own Buyer Classification series that FHBs continued to fade while mortgaged investors also stayed subdued.

In all likelihood, it's going to remain a restricted environment for mortgage activity in the coming months too (potentially creating opportunities for cash buyers and/or those reduced numbers of mortgaged buyers who have actually managed to scale the hurdles).

Sure, CCCFA is set to be eased, which will help. And the news-flow from the banks suggests that the almost-blanket ban on low deposit loans in the past few months has now started to loosen too. In addition, we've also heard that self-imposed debt to income ratio guidance at some of the banks is being removed. And given that the RBNZ hasn't been averse to easing LVR rules in the past either, who could fully rule out such a move this year too, in the event that the housing market started to slide at a faster pace (therefore potentially creating financial stability risks).

All that said, there's no escaping the fact that mortgage rates have risen and are set to increase further – by identity, reducing the amount of debt that a borrower can reasonably service. The bottom line is that 2022 will be a softer year for mortgage lending, property sales, and values.

Meet Kelvin Davidson

Chief Economist

Kelvin joined CoreLogic in March 2018 as Senior Research Analyst, before moving into his current role of Chief Economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Full profile