In today's Pulse, Chief Property Economist Kelvin Davidson discusses the sustained growth in first home buyer activity, including the outlook and market share of other buyer groups (mortgaged MPOs, movers, etc).

Movers and mortgaged investors continue to face some challenges in terms of their property purchasing decisions, although both groups are still active to some degree. On the flipside, first home buyers’ (FHBs) share of the market continues to hover at record levels, with the number of deals not too bad either. It’s clearly never easy being a FHB, but conditions look set to stay relatively favourable for this group in the coming months.

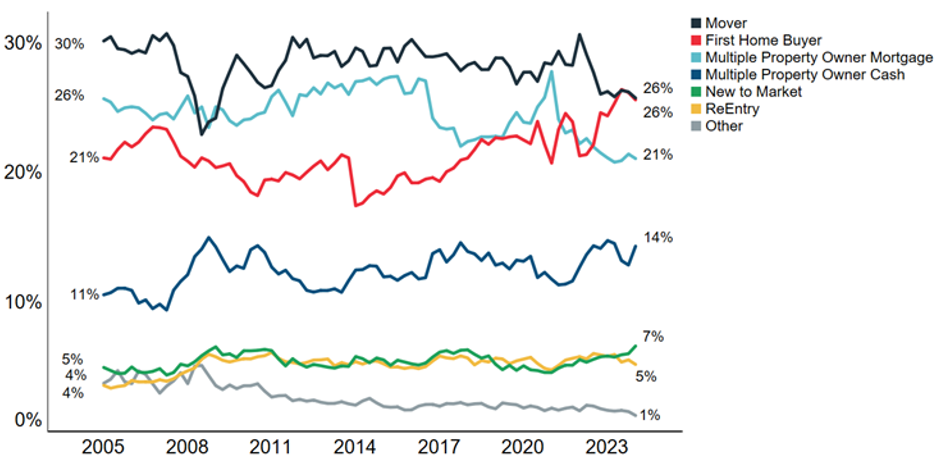

The latest CoreLogic Buyer Classification data shows that FHBs were once again a key presence in March, with a 25.6% share of property purchases across NZ. Despite the slightly earlier Easter this year (and hence fewer working days), the number of deals was pretty solid too; up by 8% from March 2023 and also slightly higher than March 2022 (but less than March 2021 when the property market was running hot). March’s result continued an already solid run of activity by FHBs, with their market share reaching 25% or more for the past year see the first chart.

Many of the main centres have had a market share figure for FHBs that is above the national average, with the Q1 2024 results for Wellington coming in at 36%, Hamilton 34%, and Auckland and Christchurch at 28% apiece. Dunedin sat at 26%, and Tauranga at 22% although compared to Tauranga’s past norms, the latest figure is actually quite strong.

There’s a long list of reasons why FHBs have been enjoying a strong presence in the market, but perhaps the most important are access to KiwiSaver for at least part of the deposit, making full use of the low deposit lending allowances at the banks (as well as targeting new builds), and of course relatively reduced activity from other buyer groups.

Indeed, the market share for movers (relocating owner occupiers) was ‘only’ 26% again in Q1 2024, the level its been sitting at for about two years now, and below a more normal figure of about 28%. The cost to ‘trade up’ not only legal and removal fees, but also the extra debt and/or equity that’s required is likely to have been a factor keeping some would be movers where they are.

We suspect that a relative lack of choice could also have been an issue i.e. would be movers simply weren’t able to find their ideal next property. Of course, now that the stock of available listings on the market has risen, this could grease the wheels a bit for movers, and see their share of purchases rise a bit in the coming months*.

1. Quarterly NZ % share of property purchases (Source: CoreLogic)

In a similar vein, mortgaged multiple property owners (MPOs, including investors) have remained relatively quiet in recent months, with just a 21% share of activity in March, and the same figure for Q1 as a whole (as well as all of 2023). To be fair, that’s still about one in every five deals going to a mortgaged investor with another 14% going to cash investors so they haven’t totally shut up shop. But there are still challenges for the mortgaged investor group in terms of low rental yields, high mortgage rates, tough deposit requirements, and the (previous) phased removal of mortgage interest deductions at tax time.

We suspect that buying ‘cheap’ properties and renovating them will have been an option for some of these investor, but clearly buying new builds is an option too given their exemption from the LVR rules and also preferential tax treatment under the previous Government (e.g. shorter Brightline and 100% deductibility for 20 years).

Indeed, as the second chart shows, we estimate that mortgaged MPOs have been accounting for more than 30% of all new build purchases in recent years, up from about 25% in 2020, the year prior to Labour’s property tax changes. (The second chart also illustrates the rising presence for FHBs in the new build market too, with relocating owner occupiers seeing a much lower market share than previous years).

Looking ahead, some factors are certainly starting to look more favourable for movers (e.g. higher stock of available listings) and also mortgaged MPOs, given that rents are rising, looser LVRs are on the cards, 80% deductibility and a shorter Brightline test (soon) are back, and also that 90 day no cause evictions are back on the table too. Indeed, breaking down the data further, there’s recently been an uptick in market share for MPO 2’s, i.e. people who now own two dwellings after their latest purchase in other words, new ‘Mum and Dad’ landlords. To be clear, the change is small. But certainly something to watch.

However, although affordability remains problematic, we’d still anticipate good opportunities for FHBs, especially if/when more low deposit finance becomes available later in 2024 (as the LVRs ease) and also because there are now more listings on the market giving finance approved FHBs more choice and increased bargaining power.

2. Annual NZ % share of new build property purchases (Source: CoreLogic)

* It does need to be noted that there’s a bit of circularity here for listings. Movers may start to sell more property, but once they’ve purchased their next house, the net effect interms of available dwellings to buy is zero.

Meet Kelvin Davidson

Chief Economist

Kelvin joined CoreLogic in March 2018 as Senior Research Analyst, before moving into his current role of Chief Economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Full profile