The Reserve Bank of NZ (RBNZ)’s final Monetary Policy Statement (MPS) for 2022 took us all by surprise – not by virtue of actually raising the official cash rate (OCR) by 0.75%, that was well signposted. More so their indication that the country’s economic outlook is worse than previously anticipated. As has been widely discussed in the media, the RBNZ now firmly expects a mild recession in 2023, which is ‘required’ to start to bring inflation down from the second half of 2023. Here I explore what else the MPS outlined, the implications for the property market, and what we should be watching for next.

The MPS indicated a peak for the OCR of 5.5% by the middle of next year, which is likely to be sustained for about a year until potential rate cuts in the second half of 2024. The RBNZ also envisages the unemployment rate rising for most of the next two to three years from 3.3% currently to around 5.5% in late 2024, due more to a larger labour force rather than outright job losses.

In terms of the property market outcomes, higher unemployment due to a rising labour force is the ‘less bad’ situation – in other words, although it’s not obviously great for prospective new buyers if they can’t find a job, at least if others (existing homeowners) aren’t losing their jobs, it means they should mostly be able to keep servicing their debts and avoid fire/mortgagee sales.

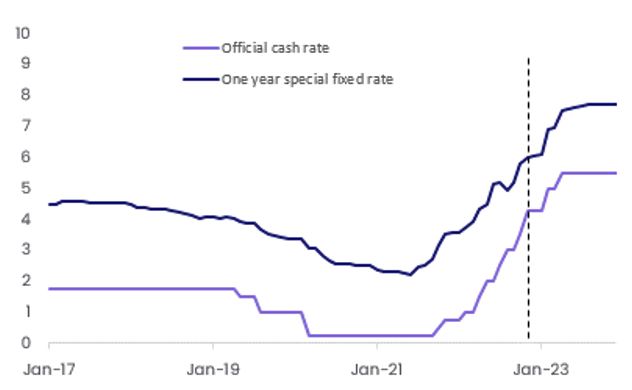

Of course, there are still many challenges ahead. For a start, an official cash rate potentially headed from 4.25% towards 5.5% – maybe via a 0.75% increase on 22 February next year and 0.5% on 5 April – implies further upwards pressure on mortgage rates, at least for floating and shorter term fixes (longer term fixes are also influenced by offshore factors).

As the first chart shows, assuming a fairly steady margin between the OCR and lending rates, a typical high-equity one-year fixed rate could easily top 7% shortly, potentially reaching 7.5% or more. We outlined the cash implications of this in a short note on Wednesday.

OCR and one-year high equity fixed mortgage rates

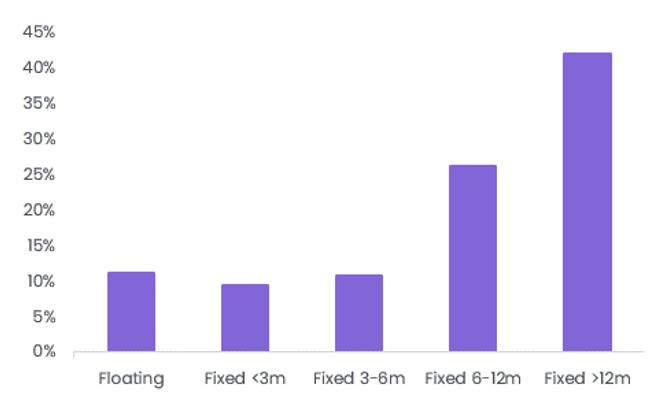

Higher mortgage rates will obviously limit the pool of potential new borrowers/house buyers, but also mean a big adjustment for existing borrowers rolling off previously lower fixed rates. Indeed, about 20% of existing loans are fixed but due to reprice in the next six months (about 10% in the next three), and 26% set to reprice within a six to 12-month horizon, see the second chart.

Share of existing mortgages by term

As an aside, with the Funding for Lending Programme due to come to an end, banks may need to increase their margin and/or find other funding to cover for the reduction in that cheap source of liquidity. That plays into the hands of term depositors. But it would simply add to the pressures on would-be borrowers and those rolling off their old, low fixed rates.

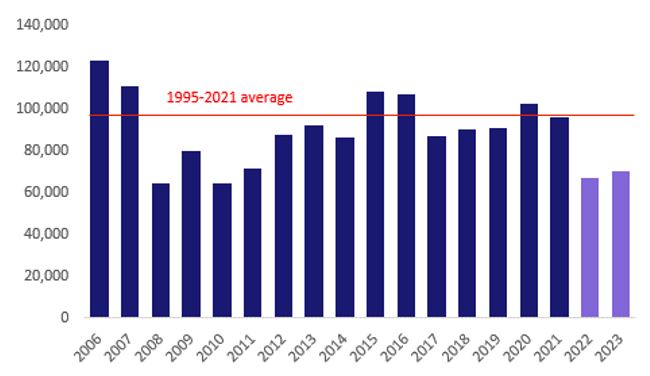

In terms of property sales volumes, our forecasting model – which uses prospective GDP growth, the change in mortgage rates, net migration, and wage growth – points to another quiet year in 2023. After a likely total of around 67,000 sales this year, activity may struggle to get much above 70,000 again next year as the economy weakens, mortgage rates remain high, but rising migration and wages provide some support (see the third chart).

Annual sales volumes

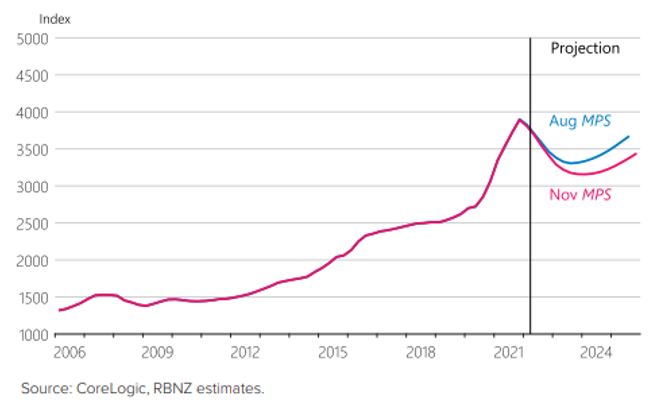

In a quiet market, it’s likely house prices have further to fall too. Indeed, using the CoreLogic House Price Index as their base, the RBNZ now envisages a total peak to trough decline in property values of 20% by the end of next year – see the fourth chart (courtesy of RBNZ). Even after such a significant decline, house prices would still be 15-20% above pre-COVID levels.

Average property values

To be fair, there may be an element of ‘tough talk’ in the latest MPS – i.e. basically the RBNZ trying to ‘scare’ inflation down without actually having to push the OCR all the way to 5.5% or tip the economy into recession. Meanwhile, we also have to acknowledge the lag between an OCR increase and the full effect on the economy, which can take at least a year. The previous RBNZ efforts, which started in October 2021, will only now be starting to bite and could really kick in early next year – signs of a deeper recession would probably keep the OCR below 5.5%.

So what are some of the key things to keep an eye on prior to the RBNZ’s next OCR decision in late February? These include:

- Any indicators of inflation expectations. The ANZ business and consumer sentiment surveys are next due on 30 November and late December respectively. If these metrics start to moderate, the RBNZ would take some comfort that their efforts so far are starting to bite.

- The next official inflation reading itself is due from Stats NZ on 25 January. Clearly, the hope (not necessarily expectation) is this might show a decline to less than 7%. For the record, the RBNZ is actually anticipating that this number might be worse than before (perhaps 7.5%), not great news for consumers in terms of living costs or their future mortgage payments.

- Stats NZ’s benchmark labour data will be out in early February and includes the latest unemployment rate and wage growth. Normally, households would want this to remain strong but from the perspective of limiting how high the OCR goes, slower wage growth might be good.

- Monthly housing market data such as our own CoreLogic House Price Index for November, which will be published on 1 December. The RBNZ will want to see a further fall in house prices, as confirmation the OCR hikes haven’t been in vain.

Meet Kelvin Davidson

Chief Economist

Kelvin joined CoreLogic in March 2018 as Senior Research Analyst, before moving into his current role of Chief Economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Full profile